Bankruptcy in Illinois: what should you do?

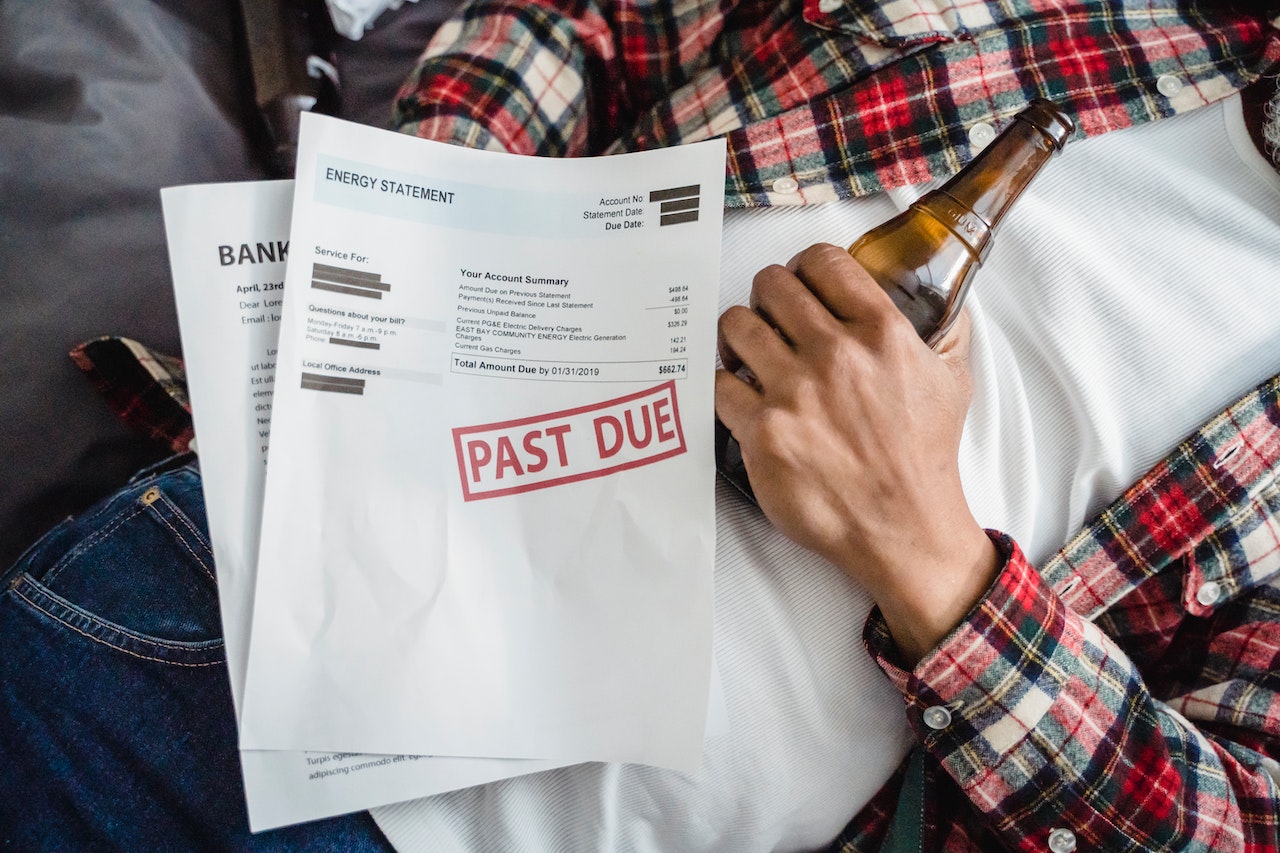

Financial difficulties are not only stressful but downright challenging. Bankruptcy is a legal process that can offer relief if you are overwhelmed by debts. But this severe matter should be considered as a last resort. Why? Because it will impact y our financial future for a long time. So, if you are considering bankruptcy in Illinois, here is what you need to know.

Types of Bankruptcy

There are different types of bankruptcy in the United States – Chapter 7 and Chapter 13. These are the two most common types for individuals and small businesses. How do they differ?

Only some people can file for bankruptcy in Illinois. There is a Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 that determines your eligibility for Chapter 7. This Act considers the state’s median income and compares it with your income and ability to settle your debts.

Some exemptions are expressly stated to protect some of your assets from being sold so you can repay your creditors. Here are some of the exemptions:

An automatic stay is a legal injunction that stops creditors from acting on your loans. They can’t foreclose, make collection calls, or wage garnishment once you file for bankruptcy in Illinois. Creditors can’t harrass you as you work through your financial situation.

The best thing to do is to look for an experienced bankruptcy attorney who can help you and guide you through your financial decisions in a crucial time like this. A legal expert can help you find other ways before filing for bankruptcy in Illinois.

Need some help with your debts? We’re here for you!

Get Free Debt AssessmentSome of the articles you can read to help manage your finances

Debt Settlement vs. Bankruptcy—which is best for you? In times […]

Read moreGet your debt settlement quote online if you face the […]

Read moreHere’s the step-by-step debt settlement process so you can easily […]

Read more